In finance and accounting, there are four financial statements that are vitally important to understanding how a business runs and how it is performing.

Here’s a brief overview of each accounting statement:

Income Statement

The Income Statement starts at the top and tells you how much a business has made in sales (or revenue), the costs of inputs for selling goods (“cost of sales”), expenses (e.g. marketing, administration costs, etc.), the interest to pay back debt, taxes and — finally — the profit.

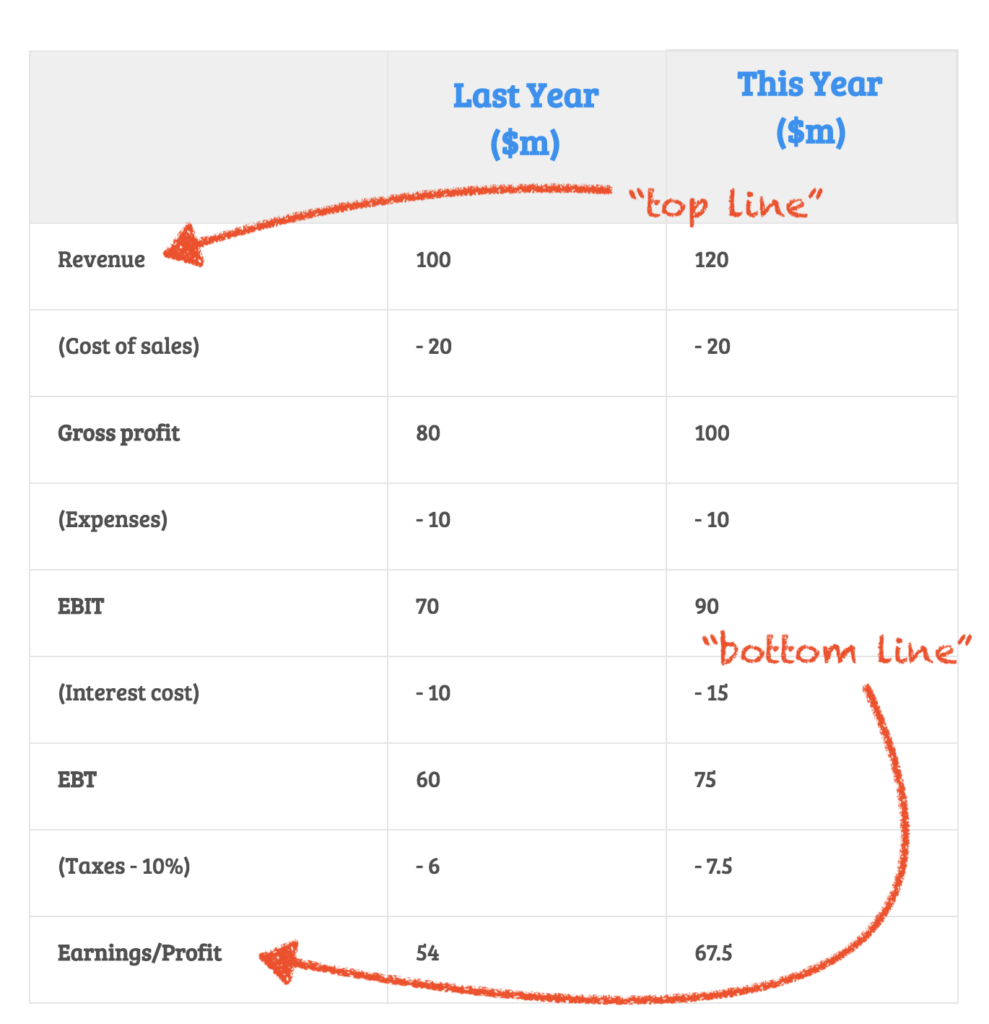

Example Income Statement

In the example above, last year, the company made $100 million in sales/revenue and incurred $20 million in costs to sell those products.

Next, it had $10 million of expenses (e.g. office costs, staff wages, etc.).

So, we have $100m (revenue) – $20m (costs) – $10 (expenses) = $70 million in profit before interest and taxes (EBIT).

The company then paid $10 million interest on its debt and paid tax of 10% (or $6 million).

So, last year, the company made $54 million in profit.

What Does That Tell Us?

We can compare the profit and sales from one year to the next year to get a sense of the direction of a business.

For example, last year the company made $54 million in profit. However, this year, the company made $67.5 million in profit — a 25% increase! That’s a big improvement on last year.

TIP: really good investors, analysts, accountants and business people will look at all of the numbers on the Income Statement to judge performance.

Ask yourself:

- Did sales rise?

- How much tax was paid?

- Did the company make a profit?

- Have I compared this company to a competitor to see which one is better?

Balance Sheet

The Balance Sheet is like a photo of a company’s financial position at one point in time.

Before we get into the details there are 4 words we need to understand.

Asset Vs. Liability

- Asset: An asset is something that makes you money (e.g. cash in the bank, a machine, vehicle, etc.). It’s a good thing!

- Liability: A liability is something you have to pay (e.g. a bill) or do for someone else (e.g. fulfil a contract to a customer).

Current Vs. Non-Current

The Balance Sheet shows you all of the assets and liabilities and then divides them into “current” and “non current” depending on when are due to the paid (liability) or earned (asset).

- Current: Current assets or liabilities will be used or paid (e.g. a bank loan) in the next year. E.g. if a company owes $15 million to suppliers that must be paid within 90 days, that’s a current liability.

- Non-Current: These are assets or liabilities that will be used or paid (e.g. a bank loan) after one year. E.g. a company owes the bank $95 million for a loan, which will be repaid over 5 years.

What Does The Balance Sheet Tell You?

Some of the important things the Balance Sheet tells you are:

- The value of the company’s assets (e.g. machinery, property, etc.)

- How much debt is owed by the company (sometimes called “long-term debt” or “interest-bearing liabilities”), and

- The amount of cash in the bank

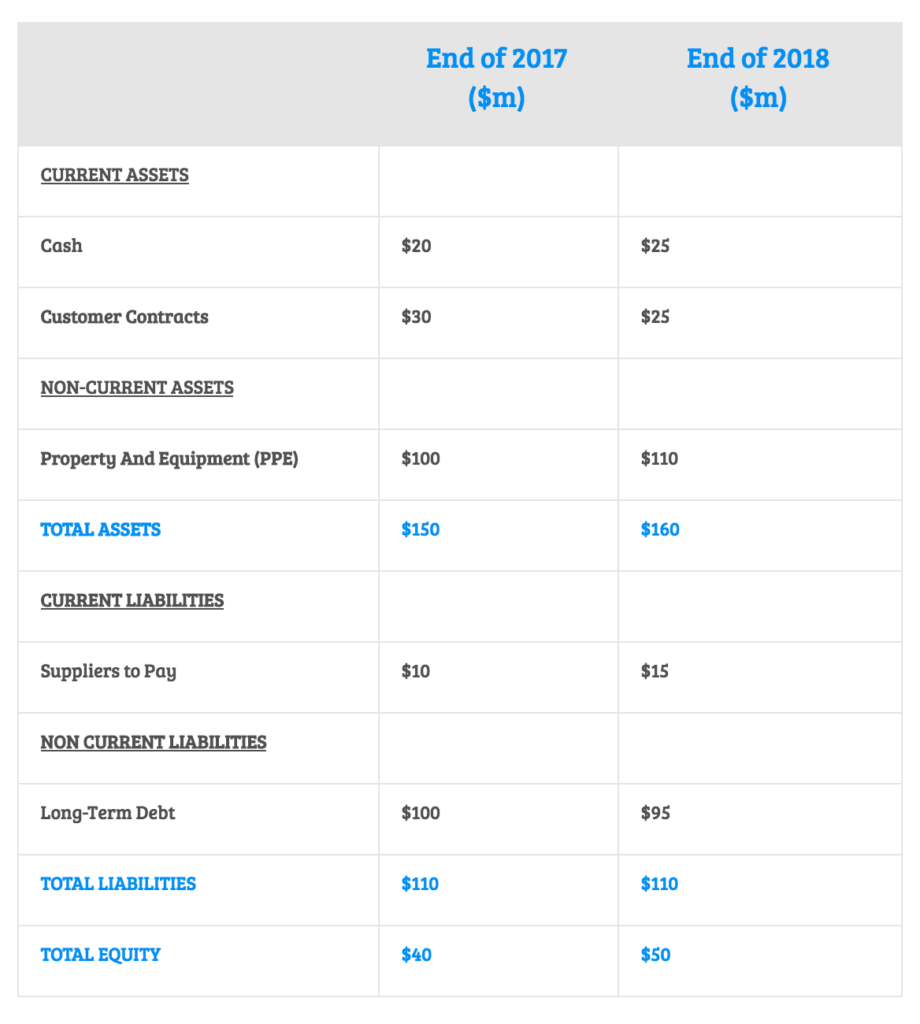

In the simple example above, the company had $25 million of cash at the end of 2018. It also has $15 million of bills to pay to suppliers.

What Is Equity?

When you’re looking at the Balance Sheet, equity simply means the difference between Total Assets and Total Liabilities. It’s just like the equity in your house.

Obviously, you want your company to have more assets than liabilities because if your company has more liabilities than assets it could be about to go out of business!

TIP: If you’re confused about an item on a Balance Sheet or Income Statement, go into the “Accounting Notes” section which can be found just after the financial statements in an annual report. The Notes include more details about each item in the financial statements.

Cash Flow Statement

We think the Cash Flow Statement is the most important financial statement of all.

The Cash Flow Statement shows you how much cold hard cash the company earned each year.

3 Sections of the Cash Flow Statement

Cash Flow to and from a company are divided into three basic sections, depending on what the cash was used for. Usually, (brackets) means cash is going AWAY from the company (a cash OUT-flow).

- Cash from Operations: this is the cash that is made and paid by the company to run its operations (e.g. cash collected from selling goods to a customer would be cash in-flow)

- Cash from Investing: This is cash received or paid to sell or buy long-term assets for the business (e.g. paying $50 million to buy a piece of property would be cash out-flow)

- Cash from Financing: this is cash used to keep the business afloat (e.g. the company gets a bank loan for $20 million, that’s a cash in-flow).

Let’s look at the three sections in more detail.

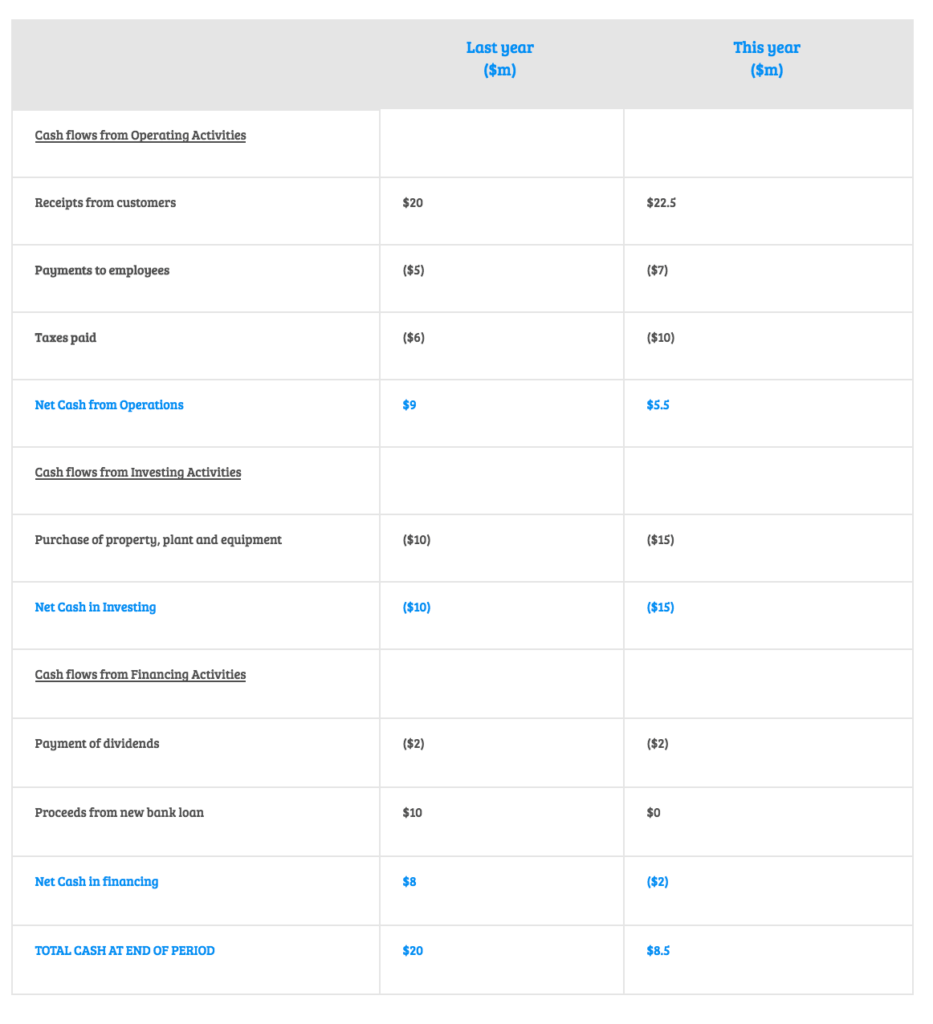

In the Cash Flow Statement above, the company made $5.5 million of cash IN-flow from its OPERATIONS this year.

Meaning, after paying its employee wages and some taxes, the company had cash leftover from the sales it made to its customers ($22.5 million).

Meaning, the company’s operations were positive, from a cash flow perspective. That’s good!

Further down under “Investing Activities” we can see that the company is investing a lot of cash ($15 million) in new property and machinery. That could be a good move for long-term growth but the company will likely need to pay for that investment with either new bank debt or existing cash reserves.

Under “Financing Activities” we can see the company paid a dividend to its shareholders ($2 million) and did NOT receive any cash from the bank this year. However, last year the company got $10 million from a new bank loan.

What Does It Mean?

If we total the 3 categories of cash flow…

- operating cash flow, positive $5.5 million;

- investing cash flow, negative $15 million; and

- financing cash flow, negative $2 million,

…we can say the company had cash OUT-flow of $11.5 million this year ($5.5m minus $15m minus $2m = $11.5m).

Because it used $11.5 million of cash and it started this year with $20 million of cash, it’s ending cash balance this year was $8.5 million. (look again at the bottom of the Cash Flow Statement and take note of the total cash at the end of last year).

If the company keeps using cash to fund its business it may soon run out!

TIP: Pay particular attention to the cash flow from operations. Is the company bringing in more cash than it is paying out? If it is generating lots of cash from its operations its business is making cash!

[ls_content_block id=”27643″ para=”paragraphs”]

{kind=link}