Here’s a run-down of the most common fees and costs associated with superannuation, as well as what to look out for.

Administration fees

Sometimes called a ‘member fee’, this fee goes to your super fund. It may be a percentage (0.5%), a flat amount ($10 per month) or capped (0.5% up to $1,000 per year). This is deducted directly from your super account.

If you have more than one super fund, you could be paying multiple administration fees and not even realise!

Investment fees

These are the fees the super fund charges to exercise care and expertise, it is usually stated as a percentage (e.g. 0.5%). Some super funds don’t charge an investment fee since the fees for investing are often included in the indirect cost ratio.

Indirect costs

These are the fees paid by your super fund to the companies that do their investments.

For example, in a ‘balanced’ investment strategy your super fund will get an investment firm to invest your money in a range of assets like shares, property, bonds, and cash. The indirect costs ratio is an estimate of the total fees to pay the investment firm.

These fees can vary slightly from year-to-year as they often include performance fees (for good investing performance) and other costs associated with the investment.

Important: Like the investment fee (above), these fees can vary depending on which investment strategy you choose (e.g. growth, defensive, capital stable, etc.).

For example, two people can have the same super fund but choose different investment strategies and therefore have different yearly costs.

Example: $50,000 Super Fund #1

| Administration fee | $100 per year | PLUS |

| Investment fee | 0.5% ($250 on $50,000) | PLUS |

| Indirect Cost Ratio (‘growth’ strategy) | 1% ($500 on $50,000) | EQUALS |

| TOTAL | $850 per year |

Using the example #1 above, if we take the total fees and costs ($850) and divide it by the balance ($50,000) that’s a total of 1.7%!

Example: $50,000 Super Fund #2

| Administration fee | $150 per year | PLUS |

| Investment fee | 0% | PLUS |

| Indirect Cost Ratio (‘growth’ strategy) | 0.5% ($250 on $50,000) | EQUALS |

| TOTAL | $400 per year |

Using the example above, if we take the total fees and costs ($400) and divide it by the balance ($50,000) that’s a total of 0.8%. That’s less than half of the cost of Super Fund #1.

Remember, fees can vary depending on which ‘strategy‘ you select (balanced, growth, defensive, etc.). If you’re confused, call the Super fund or talk to your financial adviser.

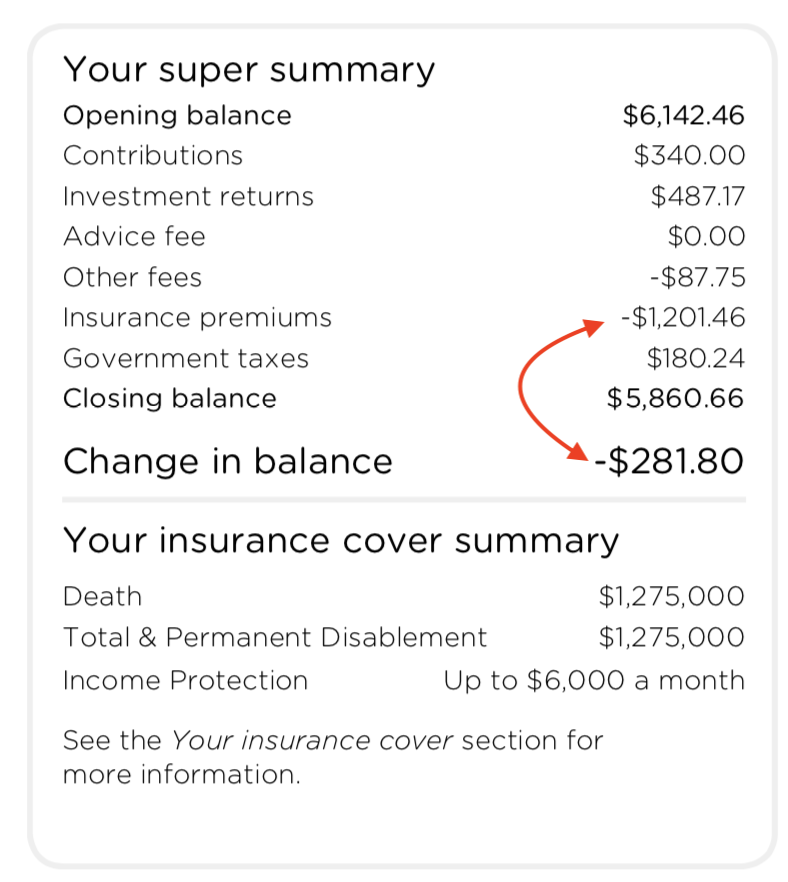

Understanding Your Super Statement

How do I check my Super fees?

Go to your Super fund’s member account/portal or read your recent statement to check your fees and costs. Typically, it will be divided into a few different types of fees.

The image above shows a Super statement and includes a line for “other fees”. These are the fees for providing the Super account, including a yearly membership fee. In this example, the investment returns ($487) are shown AFTER the investment fees have been taken out (the “investment fees” were shown in another section).

Watch out! Here are some other fees

| FEE TYPE | DESCRIPTION |

| Switching fees | Some funds charge no fees to switch between investment strategies (e.g. from ‘growth’ to ‘balanced’), but some funds will. It’s normally a flat rate (e.g. $40). |

| Advice fees | Also known as ‘financial planning fees’. This can be a flat fee (e.g. $300) or percentage (e.g. 1%). Sometimes, part of these fees can be deducted from your super account (e.g. for the advice relating to your super fund). You may also be asked to pay other fees or commissions for the advice and recommendations. |

| Buy/sell spread | These are often stated as a percentage (0.1% / 0.1%). The buy/sell spread can be used by super funds to recover the costs incurred to buy and sell investments. They are applied each time you contribute to the super fund, change investment strategy or withdraw your money. These small costs are taken out of the money that is used to buy and sell. |

| Insurance premiums | You can pay for some insurance cover inside super, with the premiums deducted from your account. Some funds have default amount of cover, but the level of cover and costs might vary. For example, you may have default level of life insurance cover inside super. If you have multiple super funds, you may be paying for many different policies! |

| Exit fees | Some funds also charge you for leaving them, this is deducted from your account when you leave. It can be a flat rate (e.g. $50) or percentage (0.2%). |

| ‘Activity based’ fees | Often, these are fees for specific actions taken by members, like information requests in a family law agreement, contribution splitting or a failure to make payment. Sometimes, these are paid from your super account, other times you (or whoever requests the information) must pay for them out of your own pocket. |

Common questions:

“Is my super fund charging me too much?”

The best way to tell if you are paying too many fees and costs for super is to compare it with other super funds.

Look at your current strategy (e.g. ‘balanced’) and compare it to another super fund using a similar strategy (e.g. ‘balanced’). Does your fund charge more or less? Remember, small differences now can make a HUGE difference when you retire.

When you compare super funds, remember that the fees can vary from one super fund to the next because the investment strategy may be different. Make sure you are comparing apples (the cost of a ‘balanced’ strategy) to apples (the second of another ‘balanced’ strategy).

In addition to fees and costs, you should also consider if the new fund offers the same, better or worse features.

How to compare

You should be able to find all the information you need — and an example of the fees and costs — in your super fund’s PDS.

To find the PDS, do an internet search for: “[your super fund’s name] PDS“. Then, search for a competitor fund to compare: “[super fund #2 name] PDS“.

Are your fees lower or higher?

Compare it to another fund.

And another.

Remember, this is your future we’re talking about.

“Where can I find my super fund’s fees?”

You should be able to find all the information — and an example of the fees and costs — in your super fund’s PDS.

To find the PDS, do an internet search for: “[your super fund’s name] PDS”. Then, search for a competitor fund to compare: “[super fund #2 name] PDS”.

“My super fund is changing its fees!”

You should be given at least 30 days’ notice by your super fund if they intend to change their fees.

“What are direct shares & ETFs inside super?“

If your super fund allows you to pick and choose which shares, Exchange Traded Funds (ETF) and Listed Investment Companies (LIC) you want to buy, you may pay other fees, like brokerage. Brokerage is usually stated as a flat rate for small amounts ($20 for investments up to $10,000) or as a percentage for large amounts (e.g. 0.1% for investments over $100,000).

In addition, ETFs and LICs may charge yearly management and/or performance fees.

It’s smart to read the Product Disclosure Statements or visit the ETF/LIC operator’s website before investing so you understand the strategy and fees for the investment.

What Does an “Investment Option” like ‘Balanced’ Actually Mean?

Before you compare your fund, it’s crucial to know what type of investment strategy or option you have selected. Watch our video in this post “How To Choose Super Investment Options”.

In that update, I explain exactly what the different choices mean and what you should look for when you’re making your decision.

[ls_content_block id=”27643″ para=”paragraphs”]