Franking credits are a tax credit available to eligible shareholders of Australian companies. They are also called imputation credits.

Woah… slow down there, partner. Imputation? Credit? Offset? Tax?!

How ATO Franking Credits work

You can think of franking credits as ‘tax credits’. Basically, if an Australian company pays tax in Australia they may be able to pay dividends to shareholders with these tax credits attached to the payment. The credits are stored at the Australian Tax Office (ATO) until a shareholder completes their tax return.

The imputation system was introduced to stop ‘double taxation’ by the ATO because if we think about it, you (as a shareholder) — are a part owner of a company. So, if the company pays tax on its profits, why should you be taxed again when the profits are returned to you in the form of a dividend?

Franking credits can have the effect of increasing a shareholder’s after-tax returns.

For example, Sarah is the only shareholder of Blue Chip Company Ltd which pays tax at 30%. It makes $100 and pays $30 as tax to the ATO. So, its profit is $70.

Blue Chip Company Ltd pays all of its profits ($70) to Sarah, including franking credits ($30). Let’s assume Sarah pays 45% tax on her income of $100. She would be required to pay $45 to the ATO. However, the company has already paid $30 tax on her behalf, so her tax payable is only ($45 – $30) $15.

Franking credits eligibility

Australian residents, self-managed superannuation funds (SMSFs) and some tax-exempt entities may be eligible to claim back the credit. However, there are some ‘integrity’ rules that shareholders should be mindful of, including1:

- The holding period rule: If a shareholder stands to receive $5,000 in franking credits (or more), they must hold the shares ‘at risk’ for 45 days (excluding the days they buy and sell). For preference shareholders the term is 90 days. For example, if Sarah buys shares today, she must hold the shares for at least 45 days (not including the day she buys and sells) to collect the franking credit at today time.

- The related payments rule: This could apply to shareholders who pass the franking credit benefit to someone else. See the ATO website or speak to tax agent for details.

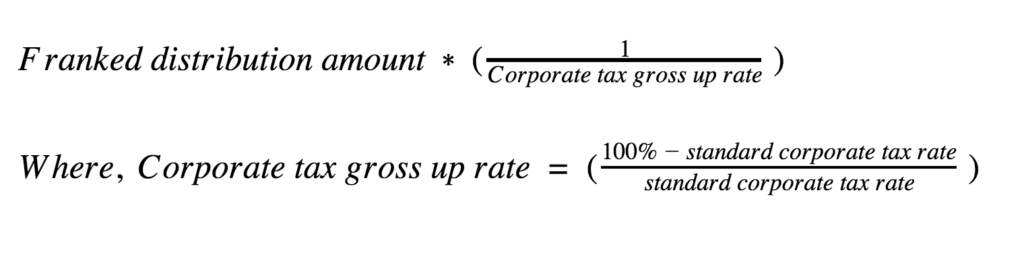

How much are franking credits worth?

Section 202-60(2) of the Income Tax Assessment Act (1997) contains the formula to calculate franking credits:

As you can see, it can get pretty ugly, so it’s best to speak to a tax agent.

What does ‘fully franked’ mean?

A company that pays 30% tax on all of its profits can pass on the full 30% of tax already paid to its shareholders. For example, if a company made $100 and paid $30 in corporate tax. It might pay $70 as dividends and the $30 in franking credits.

If a company does NOT pay 30% Australian tax on all of its profits, it may only generate enough franking credits to pay a partially franked dividend. For example, if a company earns most of its money overseas, it is unlikely to pay Australian tax on all of its profits. Therefore, it may not be able to pass the entire 30% of franking credits back to the shareholder.