Insurance policies are designed to cover us at our lowest times in life, like when we lose our good health, our house, job or car.

Key terms discussed in this video:

- Policyholder

- Life Insured

- Beneficiaries

- Premium

- Excess

- Waiting Periods

- Benefit periods

- Exclusions

- Underwriting

How to Save BIG on Car Insurance

Our epic explainer article, “4 Types of Car Insurance” explains 6 ways to save up to $500 or more on car insurance, help you identify dodgy insurers — and helps you understand which insurance is right for you. Click to read it and start saving money: “4 Types of Car Insurance.”

The “Must Read” Insurance Documents

When you take out insurance, you’ll receive two documents.

The first document is the product disclosure statement or PDS, which includes the generic terms and conditions of the insurance. The PDS should be written in plain English but it can be dozens of pages long and very confusing.

After receiving the PDS and paying for the insurance, you’ll get the second document which is called the Policy Schedule, Certificate or Document. This document is your personal certificate of insurance that has your information and other important details, like the amount of your cover and the cost of your premium.

Is [insert name] a good insurer?

Usually, the cheapest cover is cheap for a reason. If you’re considering the cheapest form of insurance:

- Do some online searches for reviews to hear the stories of other customers. Keep in mind, every insurer has bad reviews.

- Read ALL policy documents, including the Product Disclosure Statement and the policy certificate, which sets out what you are covered for and the amount.

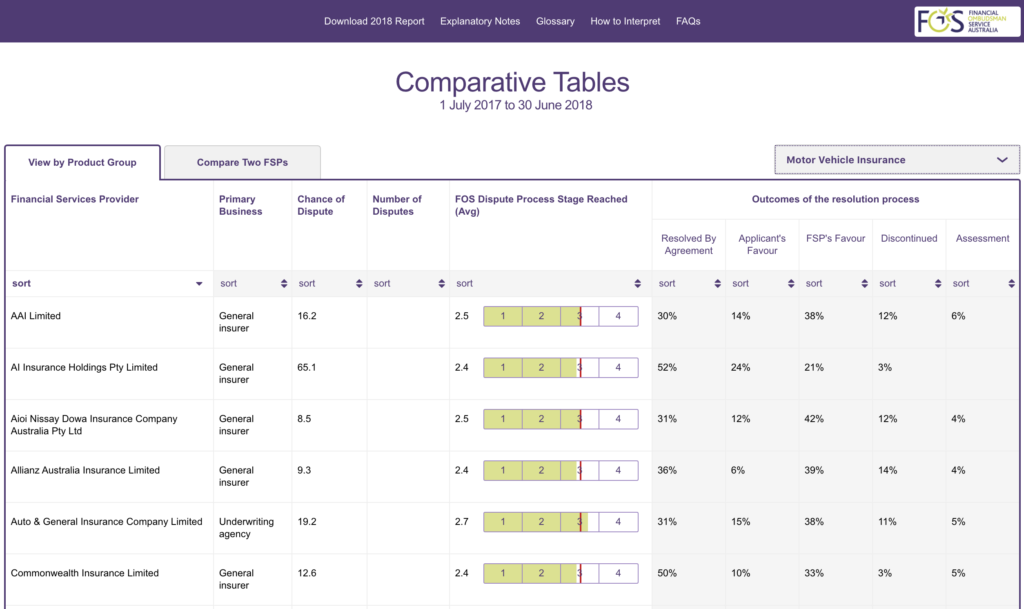

- Find your insurer in the Finance Ombudsman’s Comparative Tables. The tables tell you how many complaints or disputes an insurer has faced from annoyed customers. You know what they say, where there’s smoke, there’s a bad insurer! Tip: if your insurer ‘isn’t listed’, consider that the name of the insurer in the tables might be company behind the insurance. For example, if you bought ‘Coles insurance’ there’s another company, called the underwriter, who provides that cover — Coles is just the brand it’s sold through.

Key Terms

When you take out insurance, you’ll run into some terms that you need to know to understand what you’re signing up for.

Policyholder, life insured, & beneficiaries

The first thing to know is that the person or business who pays for the insurance is called the “Policyholder“. This person might be different to the “life insured” because you can also take out insurance on other people or property. You might also nominate other people to receive the insurance payout, they are called “beneficiaries“.

For example, a person might use their super fund to hold their life insurance and pay the proceeds to their children if they die. In this example, the person is the life insured, and the children are beneficiaries.

Premium & excess

Another two important terms are “premium” and “excess“. The premium is the amount you pay to the insurance company to take out the policy. The excess is the amount of money you agree to pay to the insurer when you make a claim.

For example, you insured your car for $10,000, which costs you $1,000 each year for the premium. Unfortunately, you get into a car accident and make a claim for the $10,000 of cover.

Before the insurer pays you the money, you will pay a fee known as “excess”, which in this example might be $500.

When you take out insurance, you can often choose a level of excess. The higher the excess you agree to pay, the lower your premium will be. That’s because you are sharing more of the risk.

Waiting periods

Some insurance policies will also mention “waiting periods“. For example, you may have to wait three months before claiming physio benefits on a health insurance policy. Generally, the longer the waiting period the lower the premium.

For example, when you take out life insurance, you may not be covered for suicide in the first 13 months.

Benefit periods

Other insurance policies, like income protection, have “benefit periods“. For example, income protection policies will replace part of your income for a period of time if you injure yourself and cannot work. The insurer will agree to a benefit period of two years, five years or until age 65. The longer the benefit period, the more your insurance will cost each year.

Exclusions

Another very important thing to note is your policy’s “exclusions“, which can be found in the PDS. Take your time to read this section because you may not be getting cover for what you want or need.

Underwriting

Finally, the term “underwriting” appears a lot in insurance policies. When you take out an insurance policy, the insurer’s medical team and financial experts will calculate the risk of your insurance cover. This is called underwriting.

For example, the insurer will use statistics and take into consideration your age, gender, smoking status, lifestyle and health to calculate the cost of your health insurance. That’s why some insurers will ask you lots of health questions and some may even ask for a medical examination before calculating your insurance premium.

Insurance is necessary but it can be confusing. Make sure you read the PDS and call the insurer to ask every question you can think of before signing up for cover.

Your future self will thank you for putting in the effort!

[ls_content_block id=”27643″]